By Piranha Profits Team

Last updated on April 07, 2026

Cybersecurity stocks are in an unusual position right now, the industry they serve has never been more critical. Global cybersecurity spending is projected to reach approximately $248 billion in 2026, growing at roughly 12.5% year-over-year, according to industry estimates building on Gartner's 2025 projections. CIO surveys consistently rank cybersecurity as a top-two budget priority. Cyberattacks are accelerating, not slowing, and naturally, investors are wondering if top cybersecurity companies (like Crowdstrike) are potentially good stocks to buy today.

And yet, cybersecurity stocks just posted one of their worst quarters in three years. The CIBR ETF, the largest cybersecurity-focused fund with over $11 billion in assets, dropped approximately 14% through Q1 2026. The S&P 500, for context, was -5% over the same period.

That disconnect is the starting point for understanding the cybersecurity investment landscape today, and for answering the question every growth investor is asking: at these prices, is the sector's biggest name, CrowdStrike, still worth buying?

Why Cybersecurity Stocks Sold Off Despite Record Demand

To understand CrowdStrike, you first need to understand what happened to the sector. Two forces converged to create the Q1 2026 correction.

The first is straightforward: valuations were stretched. CrowdStrike entered 2026 trading above 100x forward earnings. Palo Alto Networks peaked near 50x. Zscaler topped 80x. When the broader market rotated away from high-growth software names in early 2026, cybersecurity stocks (sitting at the higher end of the valuation spectrum) absorbed disproportionate damage.

The second force is the most nuanced: AI is both the biggest tailwind and the newest headwind. In February 2026, when Anthropic released a code vulnerability scanning capability, cybersecurity stocks dropped 5-8% in a single session. In late March 2026, reports of an advanced AI model with superior vulnerability-finding capabilities triggered another round of selling. The fear is straightforward: if AI-native tools can automate threat detection and response at scale, it could commoditize the very services that cybersecurity platforms charge premium prices to deliver.

But here is where the analysis needs to go deeper than the headline reaction. Because AI is simultaneously creating the largest expansion of attack surface in cybersecurity history.

The Agentic AI Paradox: Why Cybersecurity Spending Is Accelerating, Not Slowing

CrowdStrike's own 2026 Global Threat Report found that the average eCrime breakout time (the window between initial access and lateral movement) dropped to just 29 minutes, a 65% acceleration from 2024. The fastest observed breakout: 27 seconds. Attackers are deploying AI not just for phishing and social engineering, but increasingly for autonomous intrusion campaigns that adapt in real-time.

This is the paradox investors need to internalize: AI may eventually commoditize parts of the detection stack, but it is simultaneously creating an entirely new category of security demand that did not exist two years ago. The question now is whether the demand expansion from securing AI outpaces the margin compression from AI-powered commoditization.

The Winner-Take-Most Dynamic

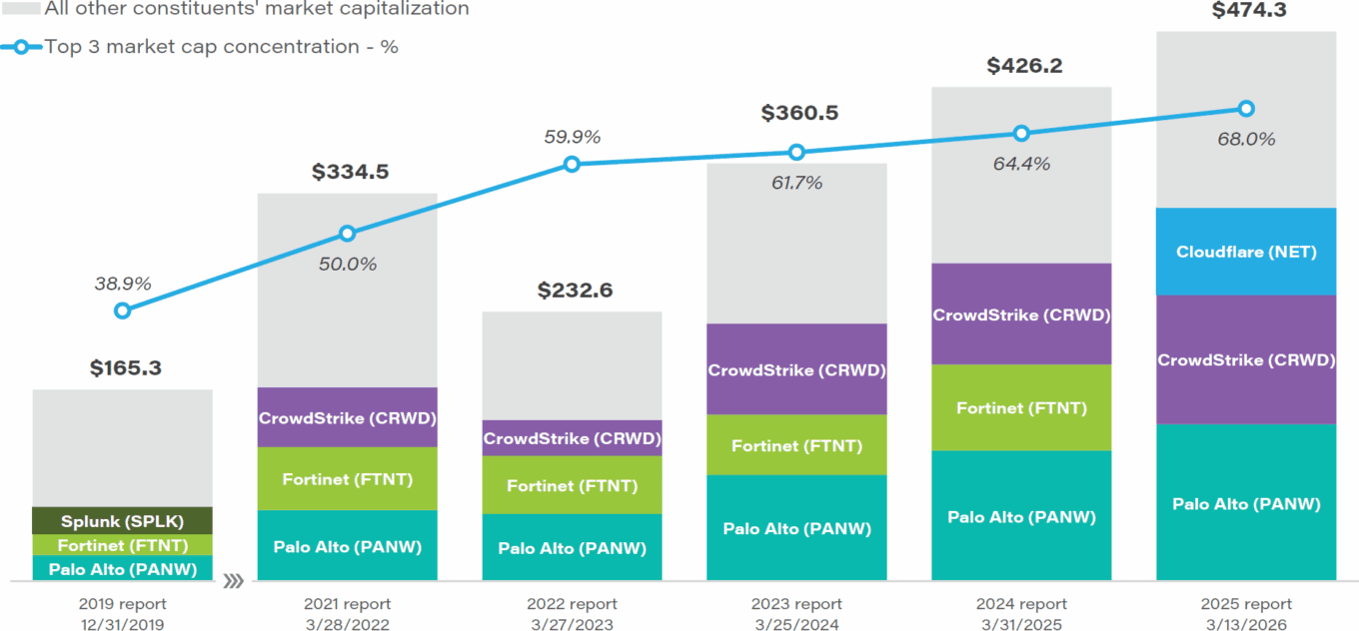

First Analysis, in their annual March 2026 cybersecurity sector report, found that market-cap concentration has reached historic levels. The top three cybersecurity companies now account for 68% of total sector market capitalization, up from 64% in 2024 and just 39% in 2019. The top four account for approximately 81%.

Meanwhile, only three out of sixteen public cybersecurity companies posted positive one-year stock returns: Cloudflare, CrowdStrike, and Radware. The median cybersecurity stock declined 18% over the past year.

First Analysis found that stock price performance showed almost no correlation with earnings beats (a correlation of just 0.02 for EPS), but showed a meaningfully higher correlation of 0.57 with expectations for future revenue growth.

It seems like in cybersecurity today, the market is paying for scale and platform breadth, not just for beating consensus. If you are investing in this sector, you might need to own the platforms that are consolidating the market.

With that framework in mind, let us examine the company that sits at the centre of this dynamic.

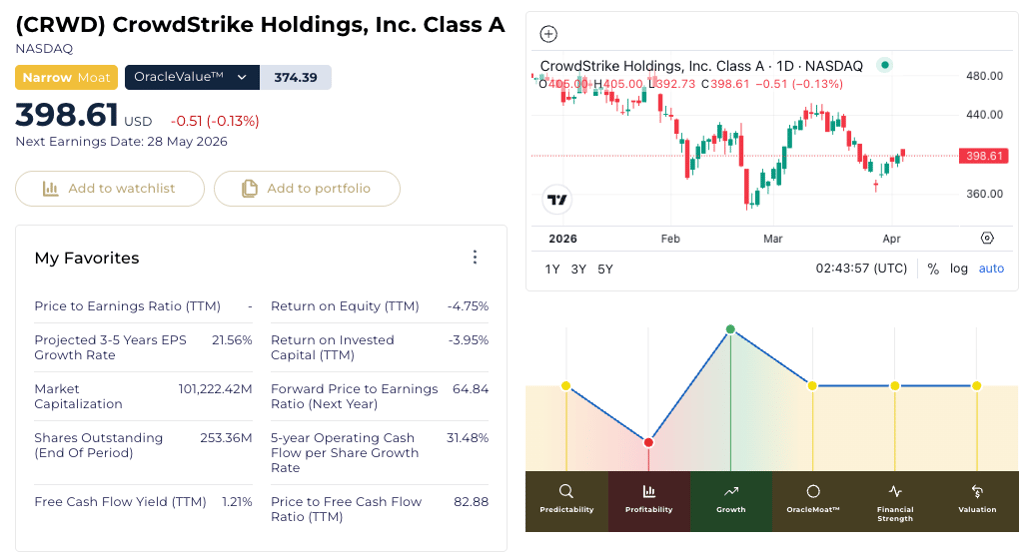

Is CrowdStrike (CRWD) a Good Stock to Buy? – StockOracle™’s Analysis

CrowdStrike (CRWD) OracleIQ™ powered by StockOracle™ — [07/04/2026]

Through StockOracle™'s breakdown, CrowdStrike looks like the classic high growth company; with strong growth profile, medium on predictability, moat, financial strength and valuations, but low in profitability (as they they still struggle to show bottom-line earnings in a sustainable way)

CrowdStrike (CRWD) Predictability Rank

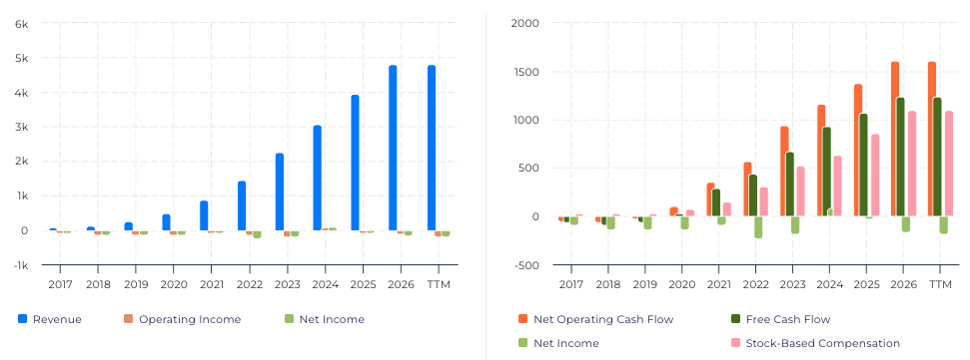

CrowdStrike(CRWD) Financials Trend Chart powered by StockOracle™ — [07/04/2026]

CrowdStrike's revenue trajectory tells a story of consistency that few software companies can match. Revenue grew from approximately $481 million in FY2020 to $4.81 billion in FY2026, a compound annual growth rate of roughly 41%.

For the full fiscal year 2026, ending ARR growth accelerated to 24% year-over-year, reaching $5.25 billion. Net new ARR reached a record $1.01 billion, the first time CrowdStrike exceeded $1 billion of net new ARR in a single year.

What makes this predictability compelling is the subscription model. Subscription revenue accounted for $4.56 billion of the $4.81 billion total, representing roughly 95% of revenue.

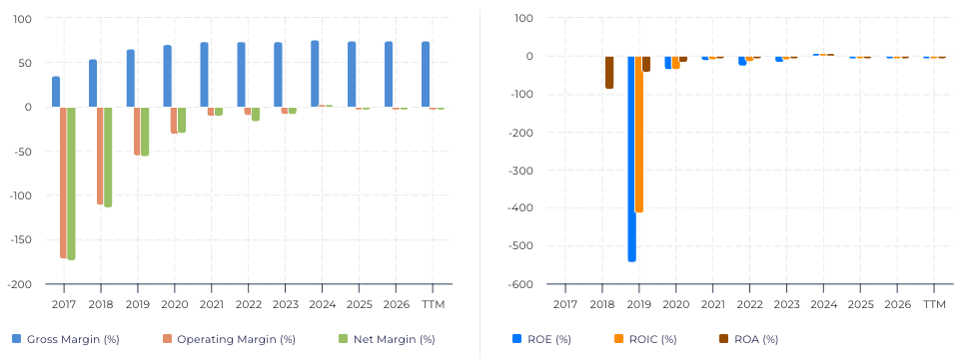

CrowdStrike (CRWD) Profitability Rank

CrowdStrike, Inc. (CRWD) Margins and Returns Chart powered by StockOracle™ — [07/04/2026]

On a non-GAAP basis, the trajectory is outstanding. Q4 FY2026 operating income reached $326 million, representing a 25% operating margin up sharply from prior years.

On a GAAP basis, however, CrowdStrike remains unprofitable. The trailing twelve-month GAAP net loss was approximately $162.5 million, driven primarily by stock-based compensation. Analysts expect the company to cross into GAAP profitability in FY2027 as operating leverage improves and SBC as a percentage of revenue declines.

CrowdStrike (CRWD) Growth

CrowdStrike's growth story has evolved. The days of 40%+ annual revenue growth are behind it. FY2027 guidance implies approximately 22% top-line growth. For a company approaching $6 billion in revenue, that deceleration is natural. The more important question is whether CrowdStrike can sustain 20%+ growth for the next three to five years.

Investors are currently looking out for their three growth engines.

Falcon Flex and the consumption flywheel. Falcon Flex, CrowdStrike's flexible consumption licensing model reached $1.69 billion in ending ARR in Q4 FY2026, growing more than 120% year-over-year and now representing 27% of total ARR. This model lets customers deploy any of Falcon's 30 modules without separate procurement cycles. The average Flex customer now represents over $1 million in ending ARR, and "reflex activity" (customers expanding their Flex commitments before renewal) nearly doubled to 10% of users, with an average 50% ARR uplift per account.

This is the growth mechanic that matters most. Falcon Flex removes procurement friction, which means upsell happens at the speed of the threat landscape rather than the speed of enterprise purchasing cycles.

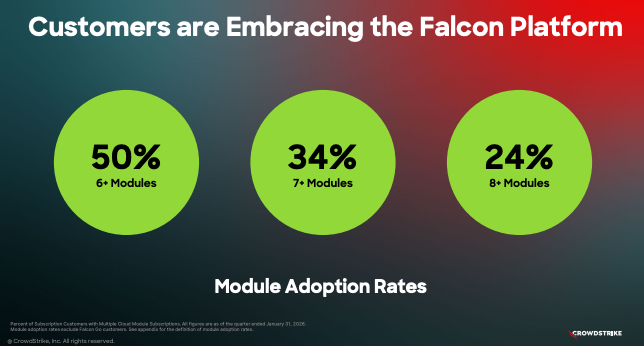

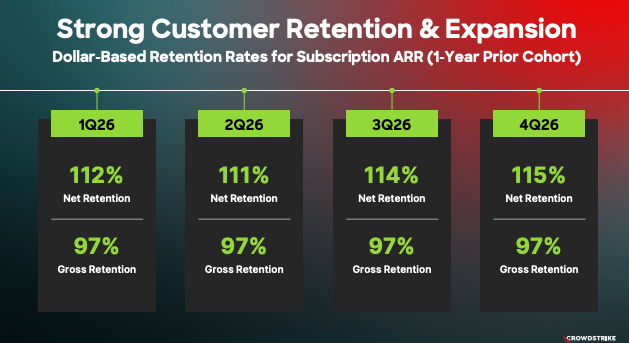

Platform expansion into adjacencies. The Falcon platform now spans 30 modules. Module adoption data illustrates the stickiness: as of Q4 FY2026, 50% of customers had adopted six or more modules, 34% had adopted seven or more, and 24% had adopted eight or more. Each additional module deepens the customer relationship and raises switching costs which explains why gross retention held at 97% even through the July 2024 global outage.

Agentic AI and the non-human identity TAM. Charlotte AI, CrowdStrike's AI assistant, is evolving from a generative chatbot into an agentic platform. Charlotte AI AgentWorks lets users build, test, and deploy custom security agents using natural language. Management's framing on the Q4 earnings call: "As enterprises rapidly adopt AI, CrowdStrike is mission-critical infrastructure, securing AI across every layer from GPU to agent to prompt."

OracleMoat™ of CrowdStrike on StockOracle™

CrowdStrike's moat rests on three pillars.

Pillar one: the platform consolidation advantage. The single-agent, cloud-native architecture means organizations can replace four to eight point-solution vendors with one Falcon deployment. This reduces complexity, cost, and attack surface simultaneously. Every additional module raises switching costs, creating a compounding lock-in effect.

Pillar two: data network effects. The CrowdStrike Security Cloud processes trillions of events per week across its installed base. This telemetry data makes threat detection faster and more accurate at scale, a classic data flywheel that is difficult for smaller competitors to replicate. Charlotte AI is trained on this proprietary dataset, which means CrowdStrike's AI capabilities are directly tied to its customer base size. More customers generate more data, which improves detection, which attracts more customers.

Pillar three: customer lock-in through operational embedding. The 97% gross retention rate through the July 2024 outage is the single most powerful proof-point for this moat. That incident, a faulty Falcon sensor update that crashed approximately 8.5 million Windows systems, disrupting airlines, hospitals, and banks globally was the kind of event that should have triggered mass defections. Net dollar retention climbed back to 115%. The outage paradoxically proved that CrowdStrike is so deeply embedded in enterprise infrastructure that even a catastrophic failure could not dislodge it.

CrowdStrike (CRWD) Valuation on StockOracle™

CrowdStrike, Inc. (CRWD) Valuation Charts powered by StockOracle™ — [07/04/2026]

Setting aside StockOracle™'s proprietary estimate, here is what the distribution of estimated valuations for CrowdStrike looks like. They currently trade at approximately $400 per share. That places it at approximately 81-91x forward non-GAAP earnings and roughly 16-17x forward revenue.

Palo Alto Networks, by comparison, trades at approximately 45x forward earnings. Fortinet trades at roughly 28x.

The 45 analysts that cover CrowdStrike stock have a consensus rating of "Buy" and an average price target of $505.93, which forecasts a 26.92% increase in the stock price over the next year. The lowest target is $368 and the highest is $613.

CrowdStrike is not cheap by any traditional metric, and the valuation leaves minimal margin for error. The February 2026 selloff saw the stock drop roughly 10% in days, demonstrating how quickly sentiment can shift at these multiples.

At the same time, cybersecurity is one of the few sectors where demand is structurally non-discretionary. Companies do not turn off their security during recessions. And CrowdStrike, as the largest pure-play cloud-native cybersecurity platform, is capturing a disproportionate share of the sector's value creation.

One way to frame the debate is that… are you paying for a company growing revenue at 22% with expanding margins and a clear path to $10 billion in ARR, with a platform moat that survived a global outage?

Or are you paying 90x earnings for a company whose growth is decelerating, and whose stock drops 8% every time an AI lab publishes a press release?

Both perspectives highlight different aspects of the investment debate, and interpretations may vary depending on time horizon and assumptions.

OracleValue™ is an estimate and should not be taken as a recommendation or a signal to buy or sell stocks.

Intrinsic value estimates are based on long-term financial projections and assume multi-year holding periods. Short-term market movements may differ significantly from valuation estimates.

Calculate the intrinsic value for CrowdStrike yourself with StockOracle™’s 7-Day Free Trial

Final Thoughts

From the StockOracle™ lens, CrowdStrike's OracleIQ™ paints a picture of a high-quality cybersecurity compounder operating at the centre of several secular tailwinds: cloud migration, AI agent proliferation, and the escalating sophistication of nation-state and criminal cyber threats.

The business is executing well. ARR is accelerating. The Falcon Flex flywheel is driving expansion revenue at scale.

The valuation, however, demands that all of this continues. At current multiples, investors are not buying what CrowdStrike is, they are buying what they believe CrowdStrike will become over the next five years.

This analysis is shared for educational purposes to illustrate how markets and valuation models react to new information. It is not intended as financial advice or a recommendation on any investment.