By Piranha Profits Team

Last updated on June 19, 2026

Palo Alto Networks reported record quarter. Q3 FY2026 revenue hit $3.0 billion, up 31% year-over-year, obliterating guidance. Yet the GAAP income statement shows an operating loss of $183 million.

A company growing at 31% with a widening GAAP loss and a trailing P/E of around 240x, the question most investors are wrestling with isn't whether PANW is growing. It's whether the market has already paid for everything that growth will deliver.

Understanding PANW's intrinsic value requires understanding its business first.

What Does Palo Alto Networks Actually Do?

Palo Alto Networks is a cybersecurity platform company.

Its platform bundles three integrated pillars: Strata (network security, including its flagship next-generation firewalls), Prisma (cloud security), and Cortex (AI-powered security operations).

The pitch to enterprise customers is straightforward: retire five vendors, consolidate onto one platform, and get better threat visibility as a bonus because all your security data now lives in one place.

The strategy is called "platformization" and it is the single most important concept for understanding PANW's financial trajectory.

When a customer platformizes, they commit meaningfully more annual spend with PANW. They also become significantly harder to displace creating a high switching cost, because ripping out an integrated platform is operationally far more painful than switching a point solution.

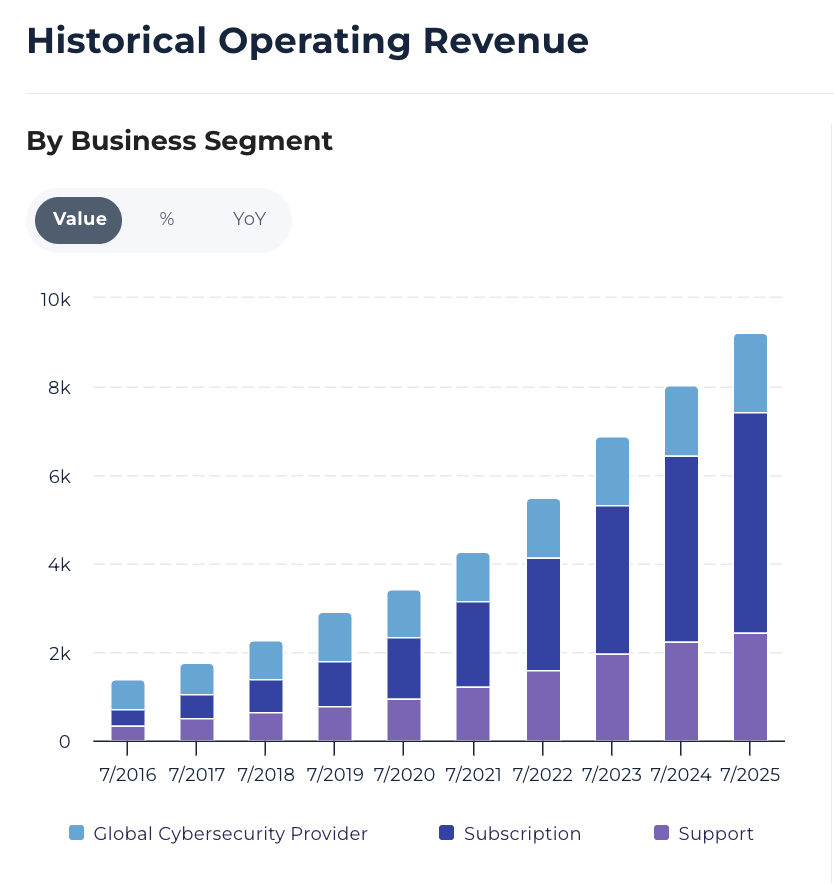

Revenue Mix: What the Charts Tell You

Looking at the historical revenue breakdown, the shift from a hardware-centric model to a recurring subscription business is unmistakable. This matters for valuation because subscription revenue is more predictable, carries higher margins, and compounds in ways that a one off product revenue does not.

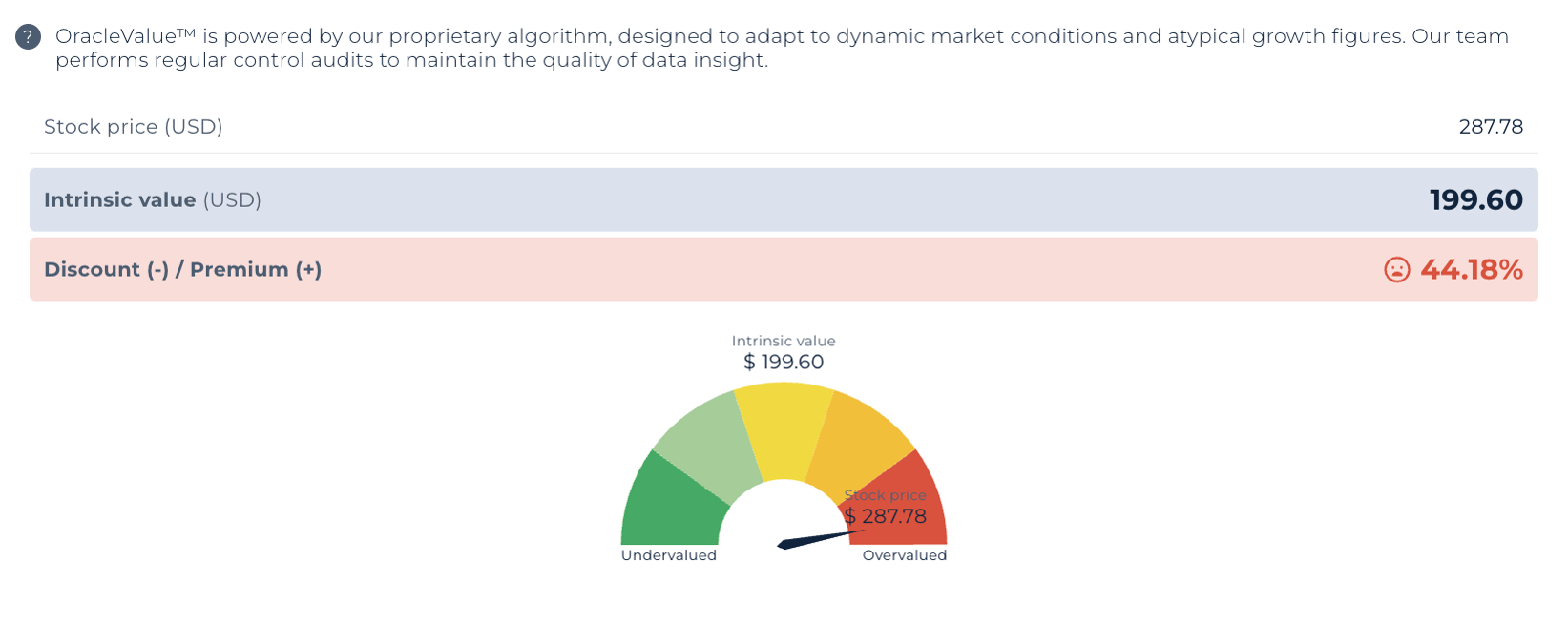

What Is PANW's Intrinsic Value?

Intrinsic value is the estimated true economic worth of a business.

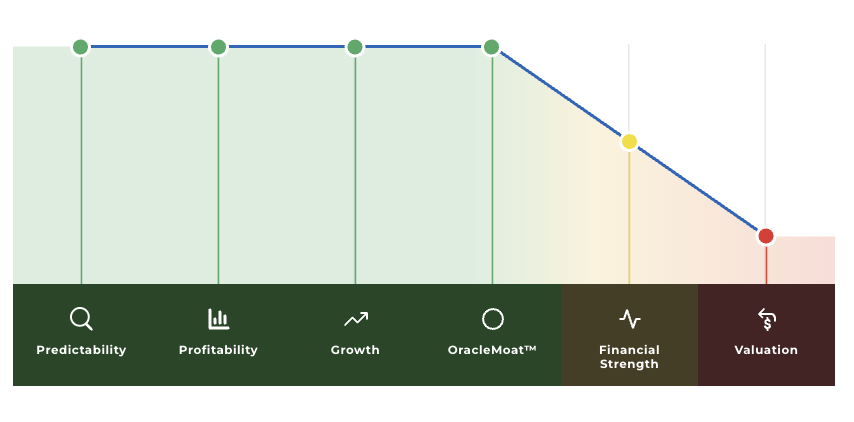

OracleValue™ estimates PANW's intrinsic value at $199.6 per share with StockOracle™ also flagging PANW as carrying a Wide Economic Moat.

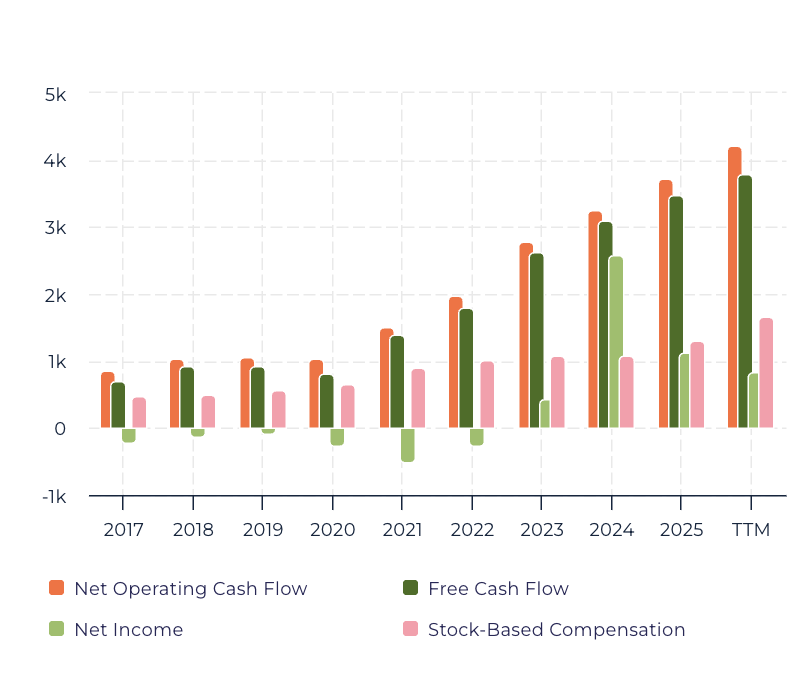

PANW's Financial Performance: What the Numbers Actually Mean

Earnings can be shaped by accounting choices. Free cash flow is the cash that actually moves through the business after every bill is paid. And Palo Alto Networks has a free cash flow margin of 35.77%

Think of it this way: for every dollar of revenue PANW generates today, it converts roughly 35 cents into real, distributable cash. As the subscription mix deepens and new customer acquisition costs are spread across a growing installed base, that conversion rate is structurally set to improve.

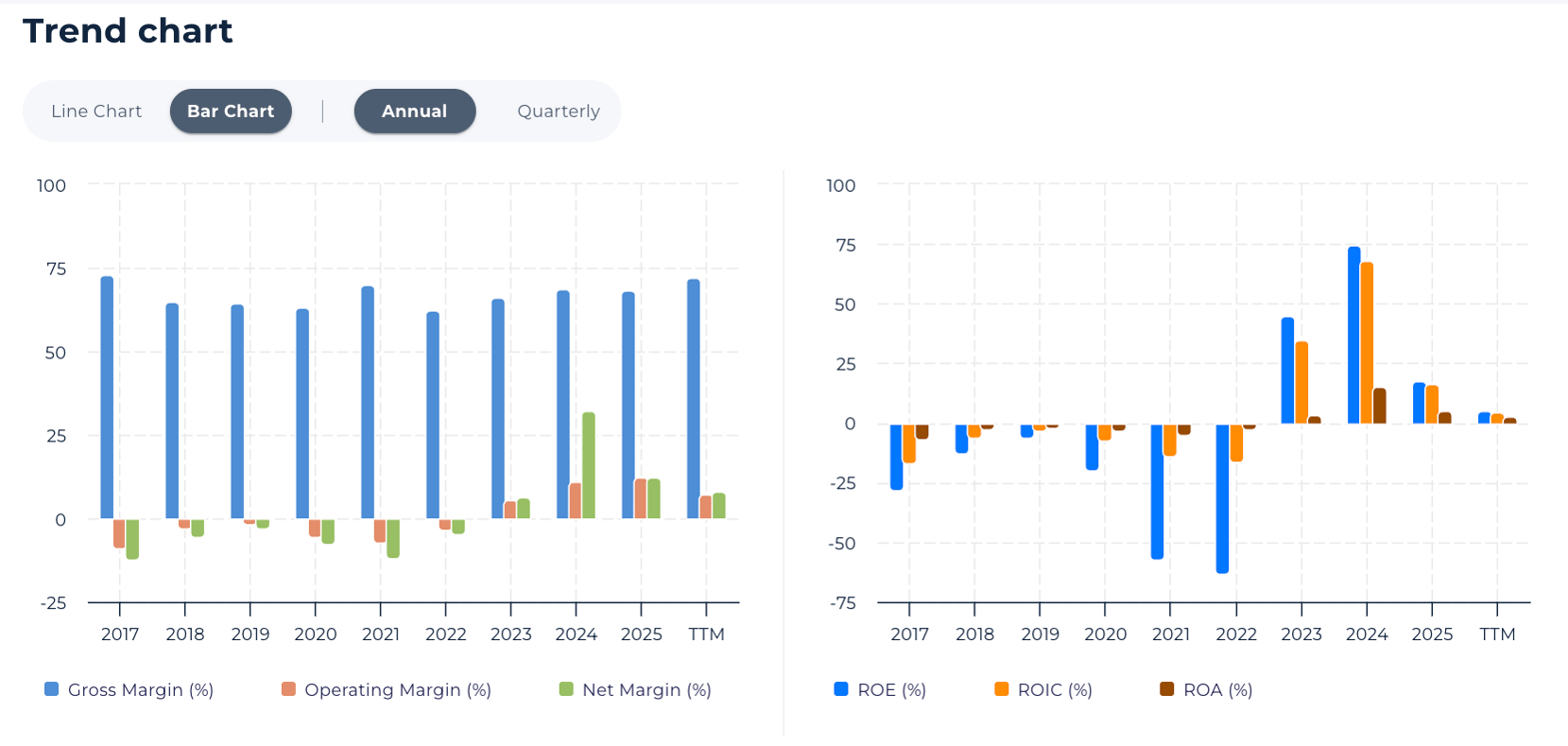

Returns Metrics: A Business in Transition

The trend chart shows a pattern that experienced investors recognise: gross margins have been remarkably stable at 65–74% across the past decade, while ROE, ROIC, and ROA have oscillated sharply. This volatility is the signature of a company aggressively investing in and acquiring capabilities.

ROIC of 4.54% (TTM) looks unimpressive in isolation. But ROIC for an acquisitive platform company reflects the capital deployed into acquisitions before integration synergies have been captured.

PANW's Economic Moat: Why StockOracle™ Rates It Wide

StockOracle™ assigns PANW a Wide Economic Moat, its highest moat rating. The moat rests on three reinforcing structural advantages.

Switching costs are structural, not contractual. When an enterprise replaces five security vendors with PANW's integrated platform, they make PANW's platform relationships deeply sticky in a way that a point solution relationship never is.

The data network effect is widening. PANW's platforms ingest security telemetry across 80,000+ enterprise customers globally, including more than three-quarters of the Global 2000. That data trains its AI threat-detection models.

The competitive geometry is asymmetric. CrowdStrike is the dominant endpoint protection platform. Zscaler leads zero-trust network access. Fortinet competes aggressively on price in SMB and mid-market firewall deals. None of these is a direct substitute for PANW's full platform.

Final Thoughts on PANW's Intrinsic Value

Palo Alto Networks is a genuinely exceptional business. The platform is sticky, the FCF engine is real, the competitive moat is wide, and management is executing ahead of schedule on one of the most ambitious acquisition integrations in cybersecurity history.

What is in question is the price as shown in OracleIQ™.

PANW is priced for a future that has to arrive. The margin for error has been priced away.

That doesn't mean PANW can't keep climbing. But it does mean the relationship between price and value has shifted. When price runs far ahead of intrinsic value, the business no longer speaks for itself. It has to keep proving itself, quarter after quarter, to justify where it's already trading.

And in that environment, any disruption matters more than it should. A guidance miss. An integration hiccup.

The business is exceptional. The price simply asks you to believe it will remain exceptional. Without interruption, without disappointment, for a very long time.