By Piranha Profits Team

Last updated on June 10, 2026

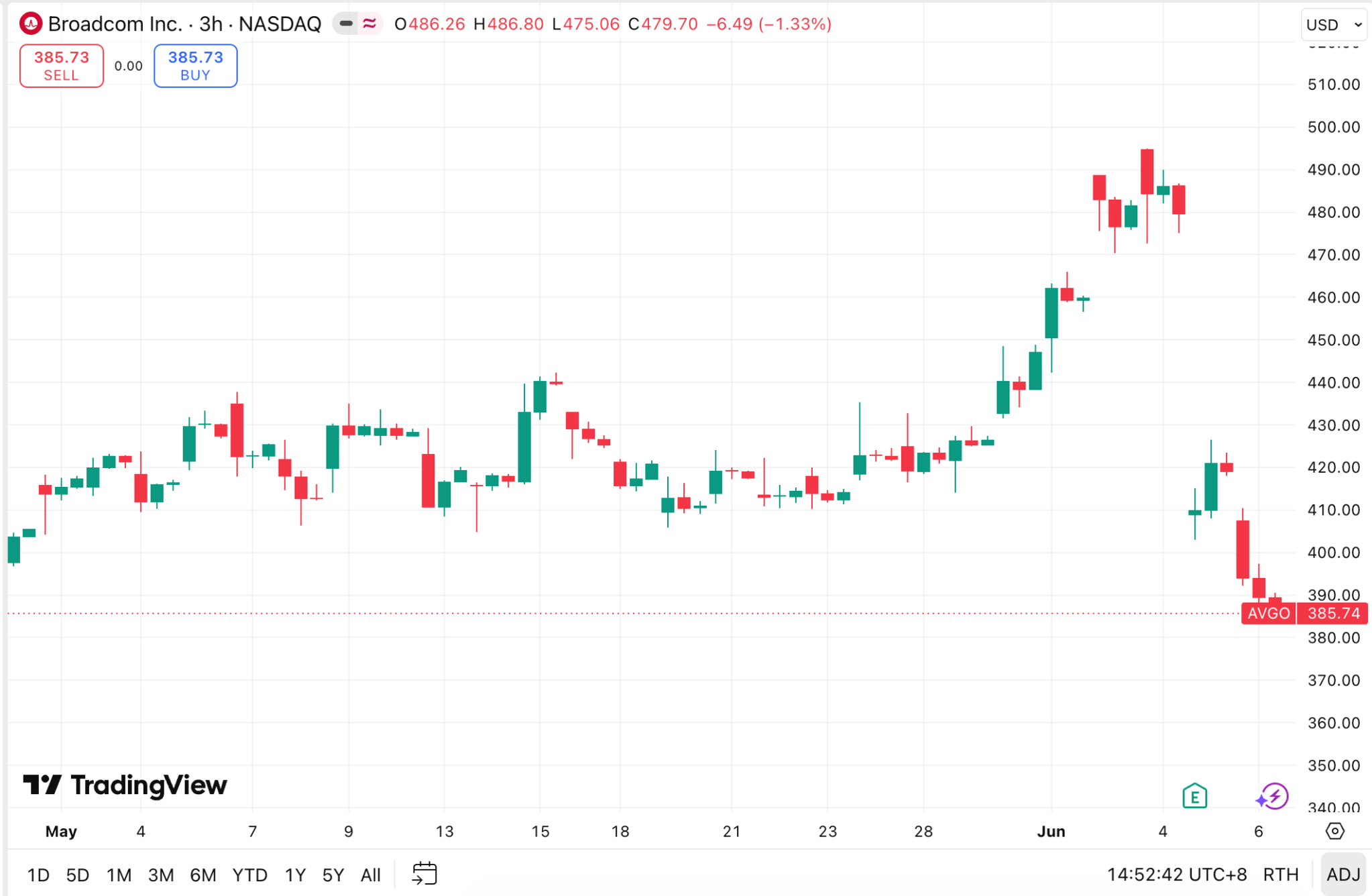

Broadcom just posted a record quarter, $22.2 billion in revenue, AI chip sales up 143% year-on-year, free cash flow of $10.3 billion. But it missed on software segment expectations ($7.18B vs $7.32B expected). And the stock fell around 13%.

|

Key Points

|

Wall Street also expected CEO Hock Tan to raise AI revenue forecast for 2027. He didn't and the market reacted.

When a stock is priced for perfection, minor news can affect its price dramatically even if the value of the stock might not have changed. That tension between price and value is exactly what makes AVGO's intrinsic value worth examining.

What Is Intrinsic Value?

Intrinsic value is essentially what a business is worth. Not what the market feels like paying for it today. While there is no fixed magic intrinsic value to any businesses, investors attempt to estimate it based on tangible value such as free cash flow, operating cash flow and multiples like the PE or PEG ratios.

StockOracle™’s AVGO Intrinsic Value Estimates and OracleIQ™

AVGO First Load Dashboard powered by StockOracle™ -10th June 2026

OracleValue™ estimate for Broadcom (AVGO) currently sits at $429.60 per share as of 6th June 2026. Suggesting the post-earnings selloff may have pushed the stock into a more interesting valuation range for long-term investors.

OracleIQ™ classifies AVGO as a Wide Moat company, reflecting the deep competitive advantages Broadcom holds in custom AI silicon and networking infrastructure, advantages that don't simply erode with a single disappointing guidance call. None of this automatically puts AVGO into "buy" territory. It does suggest that the market's reaction was more about sentiment than substance.

For investors who believe the AI growth thesis will hold over the near to long term, the OracleValue™ data points to a company that is still growing, still generating cash, and now trading at a valuation range that looks more reasonable than before the earnings call.

Broadcom (AVGO) Revenue

Broadcom's revenue has compounded steadily for a decade, but the last two years represent a step-change.

AVGO Revenue and FCF powered by StockOracle™ -10th June 2026

Q2 FY2026 came in at $22.2 billion, up 48% year-on-year driven by AI semiconductor revenue that now accounts for nearly half of total company revenue.

This isn't a cyclical spike. Bookings during the quarter hit over $30 billion against $10.8 billion shipped, which means demand is running roughly 3x supply capacity in real time.

The scale of what's coming is captured clearly in Hock Tan's own words on the earnings call: "In the second half of 2026, we expect AI semiconductor revenue to double from the first half... and for the full year 2026, we expect to achieve AI semiconductor revenue of $56 billion, up approximately 180% from fiscal 25."

That kind of revenue visibility to multi-year customer commitments with Google, Anthropic, OpenAI, and Meta is rare for a semiconductor business. Most chip companies live quarter to quarter. Broadcom is managing a roadmap that now extends into 2028.

Free Cash Flow: The Number That Actually Matters for Valuation

AVGO Revenue and FCF powered by StockOracle™ -10th June 2026

Topline growth tells you the size of the business. Free cash flow tells you how efficiently it converts that size into real cash.

In Q2 FY2026, Broadcom generated $10.3 billion in free cash flow, 46% of revenue. That means for every dollar Broadcom brought in, nearly half a dollar survived as actual usable cash after all operating and capital costs.

For a business at this scale, that's exceptional. A $100 billion annual revenue run rate combined with a 46% FCF margin would imply roughly $46 billion in annual free cash flow.

Returns: Capital Getting More Efficient as the Business Scales

AVGO Margins and Returns powered by StockOracle™ -10th June 2026

ROE, ROA, and ROIC have all trended upward over the past 18 months — a prove that Broadcom is generating more value per dollar of capital deployed even as the business scales dramatically. The Q2 FY2026 gross margin hit 67%, despite the mix shift toward lower-gross-margin AI chips. That's operating leverage working exactly as it should.

Growth Catalysts: The $100B+ Pipeline

- AI semiconductor backlog: $30B+ in Q2 bookings alone; visibility now extends to 2028

- Six contracted hyperscaler customers: Google, Anthropic, OpenAI, Meta, plus two undisclosed — all tied to multi-year XPU and networking agreements

- Networking leadership: Broadcom ships the world's only 100-terabit Ethernet switch (Tomahawk 6) and is the de facto standard in co-packaged optics — at least one generation ahead of any competitor

- Software flywheel: VMware's VCF platform is benefiting from the same GPU server boom.

- 10 gigawatt shipment plan for 2027: Management confirmed this is intact and back-half loaded, setting up a strong trajectory into 2028

Compare AVGO's OracleIQ™ against the competition on StockOracle™.

Final Thoughts on Broadcom's Intrinsic Value

The 14% post-earnings drop wasn't about the business , it was about expectations.

The market's frustration was that Hock Tan didn't raise Broadcom’s 2027 number. While the $30B quarter of bookings suggest that the demand side of that equation is getting stronger, not weaker. Investors were clearly hoping for more.

Sell-offs like this tend to create a kind of gap between price and fundamentals that value investors look for. And whether it's wide enough depends on the assumptions you're willing to defend.