By Piranha Profits Team

Last updated on May 29, 2026

|

Key Points

|

If you bought Snowflake at it's IPO 5 years ago, you're probably finally at breakeven. Yes, you read it right.

The stock that debuted as one of the most anticipated software listings in history pricing above its range, doubling within weeks and spent the next several years being quietly dismantled by rising rates, a SaaS-wide selloff, and a market that stopped paying 50x revenue for growth stories.

While the stock was drifting, the business kept building and Q1 FY2027 delivered $1.33 billion in product revenue, up 34% year-over-year, the strongest sequential dollar growth in Snowflake's history. More importantly, Snowflake is no longer just a data warehouse. With Snowflake Intelligence and its emerging data agents framework, it is positioning itself as the AI operating layer for enterprise data and the market started to reprice that possibility.

What Is Snowflake's Intrinsic Value?

Intrinsic value is what a business is actually worth based on the future cash it can generate, not what the market is pricing it at today. For a company like Snowflake, where growth has been accelerating and profitability is still maturing, the gap between market price and estimated intrinsic value can be wide and the assumptions behind that estimate matter enormously.

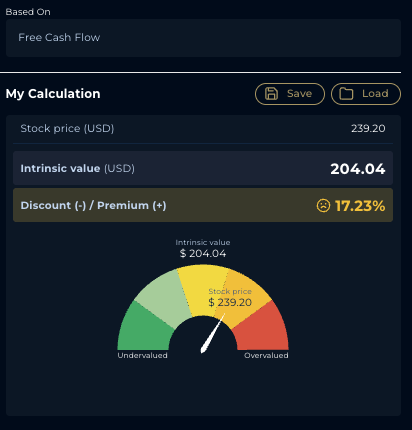

Snowflake's Intrinsic Value : The DFCF20 Estimates

Using a 20-Year Discounted Free Cash Flow model (DFCF-20), StockOracle™ estimates Snowflake's intrinsic value at $204.04 per share.

DFCF-20 Intrinsic Value Calculator — Powered by StockOracle™

The model assumes a near-term growth rate of 34.93% (Years 1–5), tapering to 8.93% in Years 6–10, and a terminal rate of 4% with a discount rate of 6.61%.

Free cash flow of $1,117.21 million serves as the base, with $4,029.69 million in cash and short-term investments added to intrinsic value, and $2,279.83 million in debt deducted. Shares outstanding stand at 337.49 million.

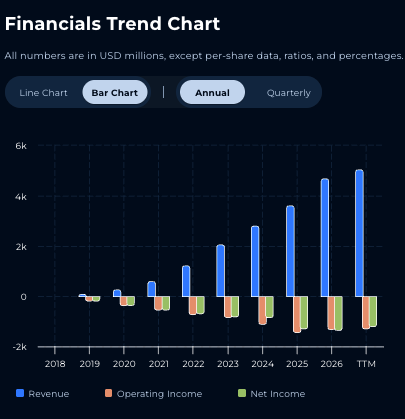

Snowflake (SNOW) Financial Performance

SNOW Revenue Trend — Powered by StockOracle™

Snowflake's Q1 FY2027 $1.39 billion in total revenue, up 33% year-over-year is the kind of re-acceleration that changes how analysts frame a growth story.

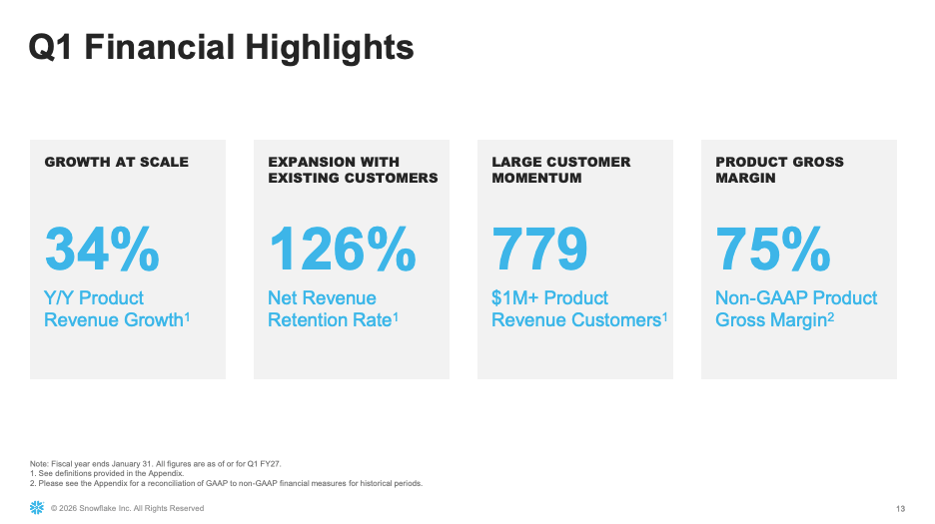

https://s26.q4cdn.com/463892824/files/doc_financials/2027/q1/Q1-FY2027-Investor-Presentation_vFF.pdf

What makes it more meaningful than headline growth alone is what's driving it: 779 customers now spend more than $1 million annually on a trailing 12-month basis, up 29% year-over-year. That's not new logo growth. That's existing enterprise accounts going deeper — the most durable, high-margin kind of expansion a platform business can produce.

The net revenue retention rate of 126% reinforces this. Every dollar of revenue Snowflake had a year ago has grown to $1.26 without counting a single new customer.

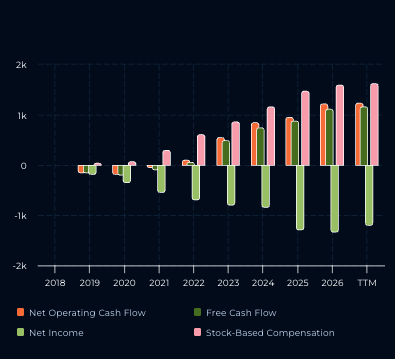

Operating Cash Flow and Free Cash Flow Chart — Powered by StockOracle™

Snowflake generated around $1.2 billion in free cash flow on a trailing basis. Basically cash left after funding every operational and capital need the business has. For a company still scaling its infrastructure and sales motion, that figure signals the unit economics are beginning to convert at scale. The higher that FCF base grows, the more weight it carries in any discounted cash flow model.

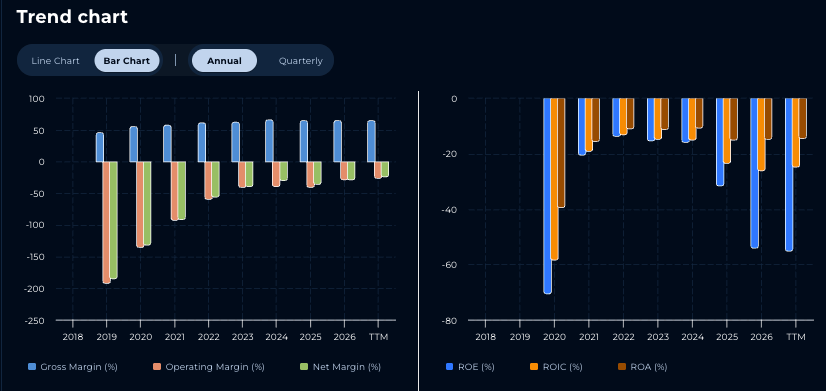

Margins and Returns Trend — Powered by StockOracle™

Gross margins have remained elevated and stable in the 60–70% range, while operating and net margins though still negative and have been narrowing consistently year-over-year.

ROE, ROIC, and ROA remain in negative territory, and each metric has been trending upward, signalling that Snowflake is extracting more output per dollar of capital as the platform scales. The inflection point from margin drag to margin expansion is the pivot the market is waiting for.

Snowflake (SNOW) Growth Catalysts

Most SaaS companies charge per seat. Snowflake charges per query, per compute, per byte processed a consumption-based model that was once seen as a liability during periods of cost optimisation, and is now being reframed as a direct lever tied to AI workload growth.

As enterprises run more AI pipelines, more inference workloads, and more data-intensive queries through Snowflake's platform, usage goes up automatically.

No new contracts to negotiate, no seat expansions to approve. The more AI workloads companies run, the more Snowflake earns. That alignment between AI adoption and revenue generation is uncommon among enterprise software companies.

Key points from Q1 FY2027:

- Product revenue of $1.33B, up 34% YoY — the strongest sequential dollar growth in company history

- 813 Forbes Global 2000 customers, deepening enterprise penetration

- Remaining Performance Obligations of $9.21 billion, up 38% YoY — contracted future revenue that hasn't hit the income statement yet

- Net Revenue Retention of 126% — existing customers expanding spend, not just staying flat

Snowflake isn't just a beneficiary of AI workloads running on its platform. It's building its own AI layer. Cortex Code and Snowflake Intelligence – announced as part of the company's Agentic Enterprise push extend Snowflake beyond data storage and processing into AI-native applications built on top of enterprise data and context.

CEO Sridhar Ramaswamy described Q1 as "a clear inflection point" for AI within the platform. With 779 customers crossing the $1M annual spend threshold and 46 of those crossing it for the first time in Q1 alone (compared to 26 a year ago), the AI product layer is already showing up in customer economics — not just in roadmap slides.

Final Thoughts on Snowflake's Intrinsic Value

The market spent years penalising Snowflake for being expensive relative to profits that hadn't arrived yet. Q1 FY2027 is the first clear sign that the model might be beginning to convert and that AI, rather than compressing Snowflake's relevance, could be expanding it.

But one strong quarter doesn't erase the memory of a 30% drawdown from IPO highs. The SaaS selloff left a mark on how investors price trust, and Snowflake now operates under a simple mandate: prove it, quarter after quarter. The thesis is compelling. The burden of proof is ongoing.

Intrinsic value estimates are based on StockOracle™ modelling and are not financial advice. Always conduct your own due diligence before making investment decisions.